Financial Exclusion

Finance is an important topic to be interpreted in all its dimensions. It could be interpreted as personal finance or the subject of finance. Personal finances in terms of income and savings are important throughout your life for everyday living and planning. Furthermore, the subject of finance is important to understand progress. Everyone can learn at their own levels; some will learn about basic finance of deposits, bonds, SIPs (Systematic Investment Plans), and mutual funds.

However, once the term “finance” is discussed, there are discussed also the problems related to it, like financial exclusion. Therefore, this report aims to have a gender-oriented both empirical and theoretical analysis of financial exclusion, especially in Italy. Why do we have this gender related analysis? Because, as expected (and verified in this report) women have more chances to be financial excluded than men, in Italy and in many of the European countries.

What is more, financial literacy will be discussed (in particular, for women and people of young age) since it will be verified that the lack of it, is correlated positively to the financial exclusion of the individuals.

Meaning of financial exclusion

The term “financial exclusion” has a broad range of both implicit and explicit definitions. Researchers mainly have proposed the following definition: “Financial exclusion refers to a process whereby people encounter difficulties accessing and/or using financial services and products in the mainstream market that are appropriate to their needs and enable them to lead a normal social life in the society in which they belong”. There is also a widespread recognition that financial exclusion forms part of a much wider social exclusion, faced by some groups who lack access to quality essential services such as jobs, housing, education, or health care.

Financial exclusion leads to social exclusion

First and foremost, financial services are an essential part of modern life in Europe and all around the world. They are needed to lead a normal life and participate equally in society. Indeed, being able to access these services is becoming so important due to technological developments.

Moreover, this need to access financial services poses a key problem of inclusion. What we mean is, that not all EU citizens and residents (taking into consideration only Europe) are currently able to use the services they need. This then has the knock-on effect of creating social exclusion, because these services are needed to meet fundamental needs such as finding employment, a place to live, and getting health care.

Higher risk for discriminated people

Certain groups of people are more susceptible to being excluded in society (and financially) in general. There are many ways to participate in society and levels of participation can depend on identity characteristics, life situations, mental and physical abilities.

Moreover, EU and international rights have been introduced to prevent exclusion arising in these cases but are not currently effective for everyone. In many, if not all, cases exclusion is closely linked to discrimination.

Furthermore, vulnerable groups can be considered as groups of people with particular features, life situations or abilities that mean they cannot enjoy the same rights and opportunity to participate in society as others. The vulnerability can manifest in different ways and affect people both throughout their lives and at specific moments.

In addition, there are a number of key barriers to financial inclusion that particular groups of vulnerable people are more exposed to. Identifying and addressing these key barriers can, therefore, have a large impact on this group, but also a wider positive impact for the other vulnerable groups affected.

Financial Literacy

The first definition we introduce is taken from OCSE- PISA 2015: “Financial literacy is knowledge and understanding of financial concepts and risks, and the skills, motivation and confidence to apply such knowledge and understanding in order to make effective decisions across a range of financial contexts, to improve the financial wellbeing of individuals and society, and to enable participation in economic life”.

Second, financial literacy is also defined by Lusardi and Mitchell (2014: 6) as: “Financial literacy is ‘peoples’ ability to process economic information and make informed decisions about financial planning, wealth accumulation, debt, and pensions”.

Furthermore, in OECD/INFE (2016: 47) the financial literacy is defined as: “Financial literacy is combination of awareness, knowledge, skill, attitude and behaviour necessary to make sound financial decisions and ultimately achieve individual financial wellbeing”.

Gender differences in financial literacy

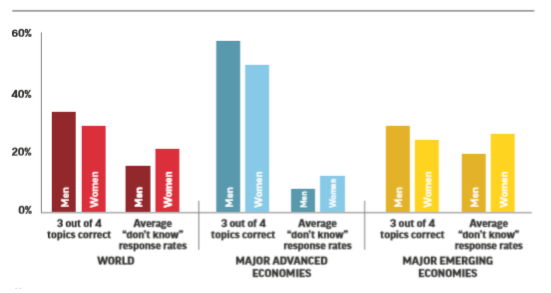

Worldwide, 35 percent of men are financially literate, compared with 30 percent of women. While women are less likely to provide correct answers to the financial literacy questions, they are also more likely to indicate that they “don’t know” the answer, a finding consistently observed in other studies as well (Lusardi and Mitchell, 2014).

Women have weaker financial skills than men even considering variations in age, country, education, and income. The average gender gap in financial literacy in emerging economies is 5 percentage points, not different from the worldwide gap. Therefore, women face a persistent gender pay gap and still occupy a very small proportion of high-income positions or senior positions. Moreover, they are much more likely than men to work part-time and typically work fewer years than men, often taking time out of the workforce to raise children or care for elderly relatives. Women have more limited access to education, employment, entrepreneurship for women than for men. What is more, there is lower financial inclusion and access to formal financial markets for women than for men. All in all, women trail men in financial literacy.

Source: S&P Global FinLit Survey

Saving for the old age and the financial literacy

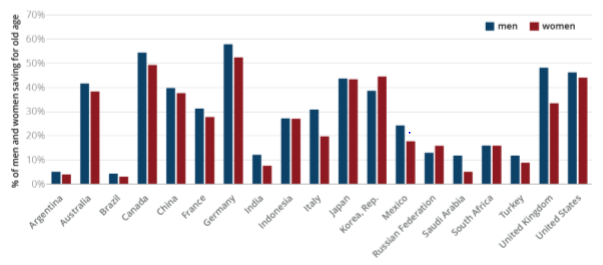

Saving for old age is a very important and difficult task for each of us. Women in Italy tend to save less for their retirement than men. Also, in many other countries men save more than women. One of the reasons this thing happens, in general, has to do with financial literacy.

Source: Evidence S&P Global FinLit Survey – 2014

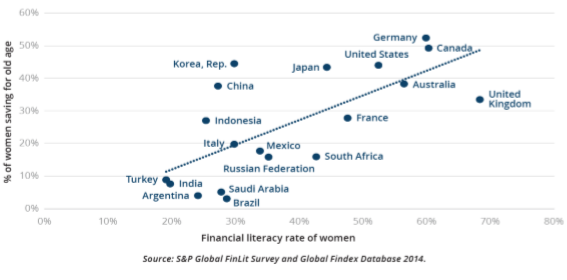

Furthermore, according to the various statistical analysis we can see that financial literacy is correlated positively to the capacity to think about the savings for the old age. Indeed, if we see the Figure down, we can notice that financial literacy among women is positively proportional to the percentage of women saving for old age. In most economies around the world, men have a better understanding of basic financial concepts than women. Thus, we can easily assume that their financial literacy is positively proportional to their percentage of saving for the old age.

All in all, financial literacy is so important to everyone, especially to women, in order to have a change in the statistical results and to empower women in this direction, also. We need to address women’s (and men’s) financial education needs through policies and dedicated programs.

Some basic alternatives could be:

1. Financial education in school

2. Financial education in the workplace

3. Financial education in the community (libraries, museums and other places where people go to learn)

Financial literacy of the youngest

To begin with, the financial literacy of the youngest is an interesting topic to be considered. For this purpose, is taken into account the Invalsi /Pisa test that also has a special contribution on financial literacy. The survey that aims to assess the extent to which 15-year-old students have acquired essential knowledge and skills for full participation in economic and social life.

Financial literacy is important for young people because students approaching the end of compulsory schooling will soon make decisions that will have significant consequences for their adult lives. Some of the examples can be deciding whether to continue their studies or whether to enter the labour market.

Some findings from the survey can be described. Compared to students with equal scores in math and reading, Italian students show a specific deficiency in financial literacy of high level. In Italy, boys score better than girls and manage to solve more complex tasks in higher percentage. In most countries OECD there are no significant differences. Italy is one of the 3 countries where there is a significant difference in favour of boys.

It is so meaningful, therefore, to ensure at least the minimum financial skills for a greater proportion of young people. Moreover, it is of high importance to encourage the acquisition of higher skills. In Italy, the gender differences in financial literacy start since a young age, as the statistical analysis presented in the survey shows.

- Financial Exclusion - August 14, 2020